Economic Theory Implies Canadian Dollar will Fall |

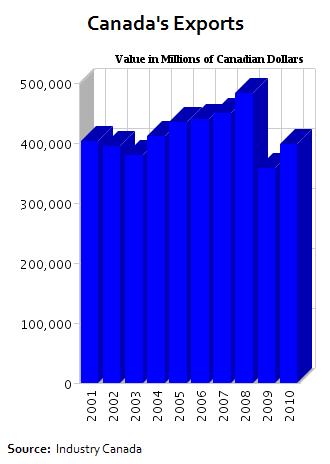

| Economic Theory Implies Canadian Dollar will Fall Posted: 25 Apr 2011 01:21 PM PDT Sometimes I wonder if I’m living in the clouds. All of my recent reports on the Canadian dollar were twinged with pessimism, and I argued that it would only be a matter of time before reality caught up with theory. While the continued surge in commodities prices has confounded everyone’s expectations, but other economic trends continue to work against Canada. In other words, I think that there is still a strong argument to be made for shorting the loonie. To be sure, the rally in commodities prices has been incredible- nearly 50% in less than a year! Oil prices are surging, gold prices just touched a record high, and a string of natural disasters have driven prices for agricultural staples to stratospheric levels. Given the perception of the Canadian dollar as a commodity currency, then, it’s no wonder that rising commodity prices have translated into a stronger currency. As I’ve argued previously, rising commodities prices are basically an irrelevant – or even distracting – factor when it comes to analyzing the loonie. That’s because, contrary to popular belief, commodities represent an almost negligible component of Canada’s economy. Canadian exports, of which commodities probably account for half, have recovered from the recession lows of 2009. On the other hand, the value of Canadian exports are basically the same as they were 10 years ago, when one US dollar could be exchanged for 1.5 Canadian dollars.

One area that higher commodities prices will be felt is inflation, which is nearing a two-year high and rising. At 3.3%, Canada’s CPI rate is now higher than in the EU. Given that the European Central Bank hiked rates earlier this month, it probably won’t be long before the Bank of Canada follows suit. In fact, forecasters expect the benchmark rate to rise by 50-75 basis points by the end of the year, from the current 1%. This might excite carry traders, but probably few others. Besides, given that other central banks will probably raise rates concurrently, it can’t be assumed that carry traders will automatically gravitate towards the Canadian dollar. Not to mention that as I pointed out in my previous post, the carry trade is hardly a risk-free proposition. In this case, an interest rate differential of only 1-2% probably isn’t enough to compensate for the risk of a correction in the USD/CAD. And that is exactly what I expect will happen. The fact that the loonie has shattered even the most optimistic forecasts is not cause for bullishness, but rather for concern. According to the most recent Commitment of Traders report, net long positions are reaching extreme levels, and it’s probably only a matter of time before the loonie returns to earth.  |

{kind=link}

{kind=link}

{kind=link}

| You are subscribed to email updates from Forex Blog To stop receiving these emails, you may unsubscribe now. | Email delivery powered by Google |

| Google Inc., 20 West Kinzie, Chicago IL USA 60610 | |

No comments:

Post a Comment